Boots vs. Bombs

March 3, 2026

It’s Tuesday morning, and we won’t be rehashing details of the events. There’s a lot of great content out there to put things into perspective from folks who know tons more about waging war, the political dynamics of the region, and/or the states/people involved. Instead, we’re going to talk markets, because we’re portfolio managers, not fighter pilots. My wife knows one who is both, but it’s rare.

Markets managed rather well on Monday. After a weak start for the first trading day since hostilities broke out, North American markets managed to finish in the green. Oil was up, as were safe havens, including gold and the USD. Tuesday looks like another weaker start, with everything down from overseas markets to bonds, gold to North American equities. Rebounding from this one may be an even bigger challenge. The U.S. dollar and oil are just about the only things higher.

Why the Initial Muted Response From Markets?

#1 The conflict is not really a surprise – Tensions had been building over the past few months and weeks, with military assets increasingly moved into the region. Add this to a U.S. administration that appears to want to use its military more, and the surprise would have been if there wasn’t a conflict.

Markets generally move when surprised. Perhaps Iran’s retaliation on some of its neighbours is a bit of a surprise, or a few signs that the conflict is spreading. More U.S. casualties would have been a negative surprise, as would the targeting of energy infrastructure, which is possibly starting to show up now. The magnitude is clearly greater than the brief bombing of nuclear development sites last year or the Iran-Israel missile exchanges of April 2024, but so far, not many surprises.

Obviously, this can change; that’s why they are called ‘surprises.’

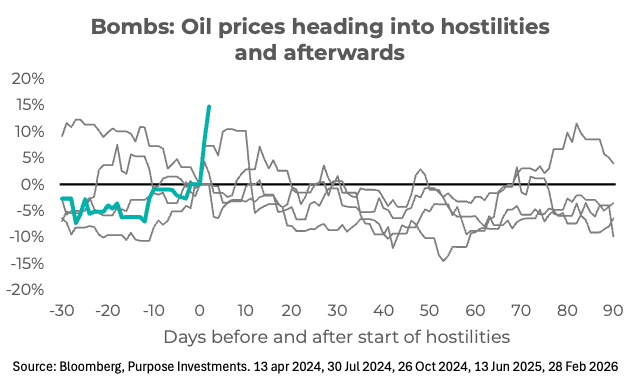

#2 A learned response of boots versus bombs – The market remembers, with short-term memory much more dominant than long-term. Putting boots on the ground leads to much longer and more painful market reactions. Dropping bombs can end as quickly as it started.

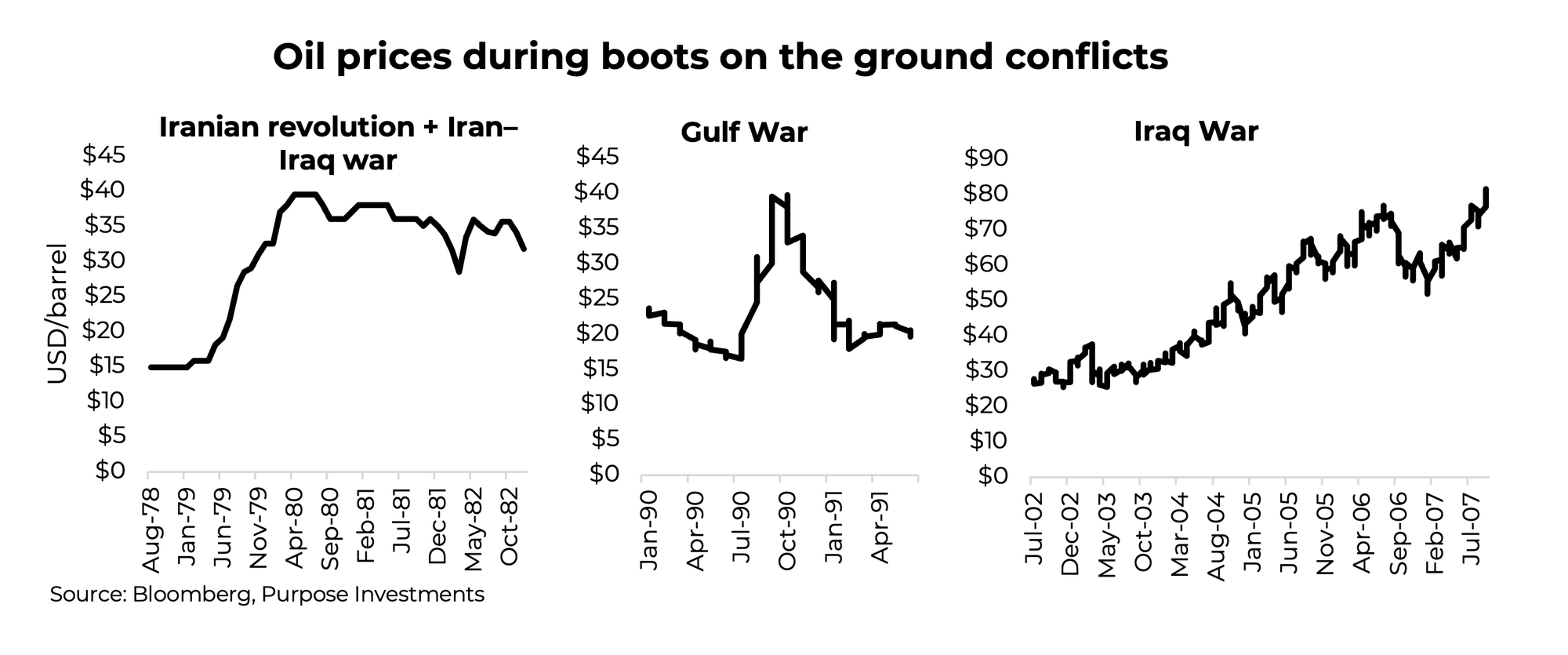

The following chart shows the past five times Iran has been bombed and the path of oil prices. The turquoise line is the current situation, already off to a bigger start than past episodes. The general trend is for a spike, then oil prices come back down. It’s a very different chart if you go back in time to boots on the ground in the next set of charts, which had often seen a doubling of oil prices.

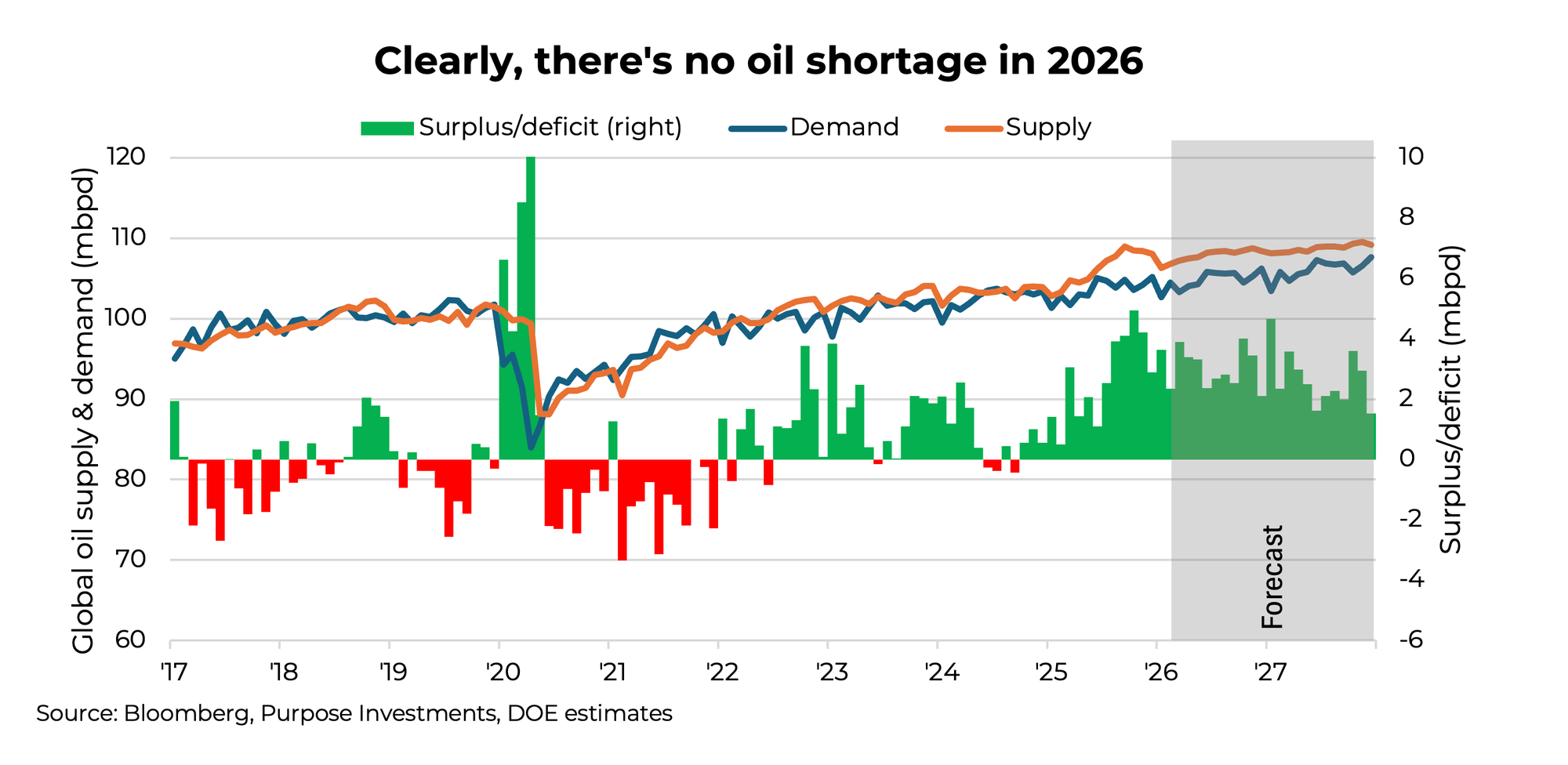

One reason the energy markets may endure this supply disruption a bit better is the amount of global supply versus demand. A surplus of two million barrels a day certainly makes managing a temporary supply disruption much easier.

One reason the energy markets may endure this supply disruption a bit better is the amount of global supply versus demand. A surplus of two million barrels a day certainly makes managing a temporary supply disruption much easier.

Final Thoughts

Final Thoughts

We don’t know how this conflict plays out; it could be short or it could become drawn out. Nobody knows. The longer it goes on, the higher the probability of a risk-off event, which may be a buying opportunity given the economic backdrop. As the Chinese proverb goes: “We’ll see.”

— Craig Basinger is the Chief Market Strategist at Purpose Investments

Sources: Charts are sourced to Bloomberg L.P.

Disclaimers

The contents of this publication were researched, written and produced by Purpose Investments Inc. (PII) and are used by Foundation Wealth Partners for information purposes only.

PII is part of the of the corporate group of Purpose Unlimited Inc., which also includes FWP’s affiliated service provider Advisor Solutions by Purpose.

This report is authored by Craig Basinger, Chief Market Strategist, Purpose Investments Inc.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by the author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Foundation Wealth Partners warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.