Foundation Wealth: The Market Just Did Something It’s Only Done 13 Times Since 1950

May 6, 2026

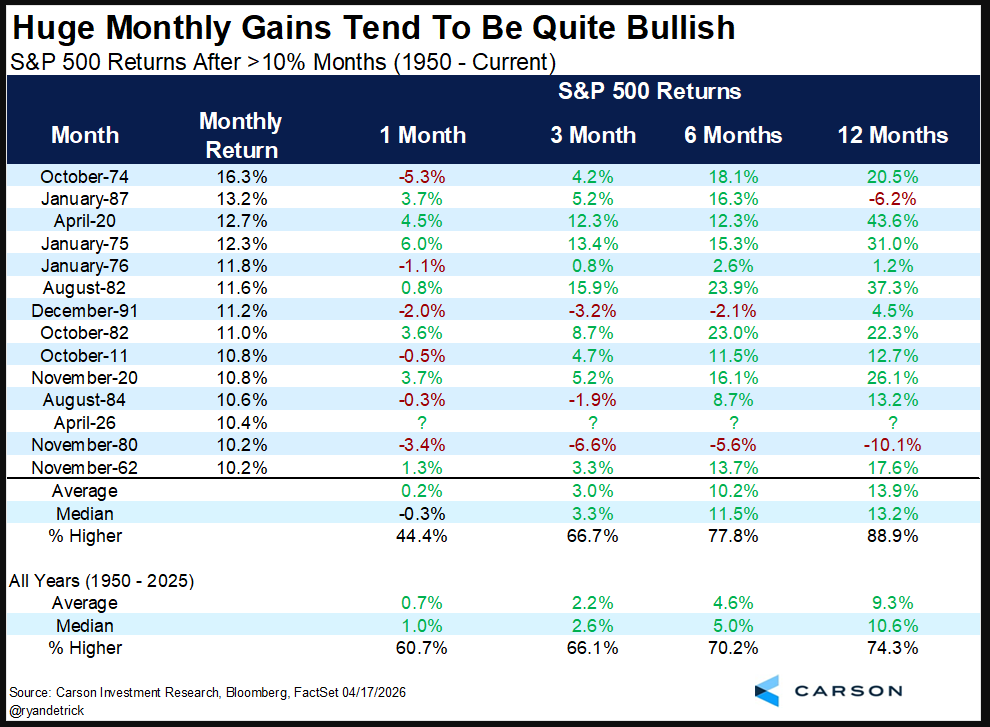

The stock markets have been on an incredible run. The S&P 500 surged 10.4% in April — only the 13th time since 1950 that the index has gained more than 10% in a single month. Historically, when that has happened, the market has usually continued moving higher. In fact, out of the previous 12 occurrences, the S&P 500 was higher a year later 10 times.

Markets continue to be driven by two major themes right now: the short-to-medium-term geopolitical risks surrounding Iran and the longer-term structural growth story around artificial intelligence.

On the geopolitical side, the market remains focused on the ongoing standoff involving Iran, the United States, and the Strait of Hormuz. While energy prices have risen, I continue to believe the biggest concern is not necessarily crude oil itself. Historically, capitalism has a way of adapting — higher prices eventually incentivize new production, alternative suppliers, and shifting trade flows. We have seen this repeatedly over decades in commodity markets.

Where I believe the larger risk exists is in liquefied natural gas (LNG) and agricultural inputs, particularly fertilizers. Fertilizer production and distribution are much harder to replace quickly, and disruptions can have ripple effects through the global food supply chain. Europe remains heavily exposed to LNG availability, while many emerging market countries are vulnerable to higher agricultural and food costs.

Wealthier countries such as Canada and the United States will likely absorb these pressures through higher prices rather than outright shortages. Poorer nations, however, may face much more severe consequences, including food inflation, factory shutdowns, and energy shortages. History has shown that developed economies generally have a far greater ability to tolerate and absorb rising prices, even if consumers feel stretched financially.

That said, prolonged uncertainty is still not ideal for markets. The longer this geopolitical stalemate drags on, the more likely it is that higher energy and transportation costs begin feeding into inflation expectations again. My hope is that supply chains — particularly around LNG and agricultural products moving through the Strait of Hormuz — normalize before these pressures become more entrenched.

Ironically, periods like this also tend to accelerate long-term structural changes. One of the clearest examples is energy security. Countries and corporations around the world are realizing that relying too heavily on single supply routes or unstable regions creates enormous vulnerabilities. As a result, nations are actively diversifying supply chains and forming new trading relationships.

This is one reason we are becoming increasingly constructive on Canada over the long term. Canada possesses abundant natural resources, political stability, and close relationships with Western allies at a time when reliability matters more than ever. Recent export strength in areas such as oil and gold reflects this trend. The world is no longer searching only for the cheapest supplier — it is searching for dependable suppliers. In many ways, that shift plays directly into Canada’s strengths.

On the investment side, artificial intelligence remains a dominant long-term theme in our portfolios.

Over the past year, many investors became increasingly worried that the AI trade had become a speculative bubble. That concern peaked last fall when several companies tied to the space experienced sharp corrections and many investors began questioning whether the entire AI narrative had gone too far.

What we are seeing now, however, is a much more nuanced environment.

Software companies tied to AI have undergone a significant downward repricing. In many cases, valuations have compressed meaningfully as investors reassessed which companies truly benefit from AI and which ones may face disruption from it. In our view, parts of the software space are beginning to look increasingly attractive again from a valuation perspective.

At the same time, the large technology infrastructure companies — the hyperscalers and semiconductor leaders powering the AI buildout — continue to post extremely strong earnings and profitability. Demand for AI infrastructure, computing power, electricity, and data center capacity remains robust.

Importantly, the current market environment does not resemble the euphoric conditions typically seen near major market tops. Despite equity markets reaching new highs, investor sentiment remains surprisingly cautious. Conversations continue to center around taking profits, fears of recession, geopolitical risks, and concerns that markets have moved “too far too fast.”

Historically, major bubbles tend to peak when optimism becomes universal and speculative behavior becomes excessive. Today, we are still climbing what is often referred to as a “wall of worry,” where investors remain skeptical even as markets advance.

One area we continue to focus on heavily is energy infrastructure tied to AI. The world is rapidly discovering that electricity — not chips — may ultimately become the biggest bottleneck to AI expansion. Building massive data centers and AI infrastructure requires enormous amounts of power, and it must be delivered quickly and affordably without dramatically increasing local electricity prices.

That creates opportunities well beyond traditional technology companies.

While natural gas and LNG will likely remain an important bridge fuel in North America, renewable energy sources such as solar are currently among the fastest and easiest solutions to deploy at scale. At the same time, there are major shortages in the equipment needed to convert energy into usable electricity infrastructure, including turbines, electrical components, transmission systems, and grid upgrades.

As a result, many of the investment opportunities tied to AI are not necessarily pure software companies, but rather the “picks and shovels” businesses building the infrastructure underneath the AI boom. This includes areas such as industrial manufacturing, electrical infrastructure, engineering, construction equipment, and power management. Companies involved in building data centers, upgrading electrical grids, and supplying industrial equipment stand to benefit from the enormous capital spending now underway.

We are also seeing attractive opportunities in select emerging markets. Countries around the world are effectively participating in the same AI race currently taking place between the United States and China. Rather than attempting to predict a single winner, our approach is often to focus on the broader trend itself — following where governments, corporations, and capital are aggressively investing.

For these reasons, we continue to remain constructive on equities overall.

Within portfolios, our primary positioning continues to focus on long-term themes surrounding AI infrastructure, energy security, agriculture, electrification, and industrial buildout. While these sectors have experienced some volatility, we avoided panicking during periods of weakness and also resisted aggressively chasing momentum higher. So far, that balanced approach has served us well.