Halftime: What We're Watching as We Enter the Second Half of 2026

July 3, 2026

The end of June marks halftime for the 2026 investment year and so far, so good.

Many investors entered the year heavily concentrated in the Magnificent Seven (Apple, Microsoft, NVIDIA, Amazon, Alphabet Meta, Tesla) but so far, these stocks have significantly underperformed the other 493 companies in the S&P 500. For anyone with a diversified portfolio like we do, this has actually been a positive development.

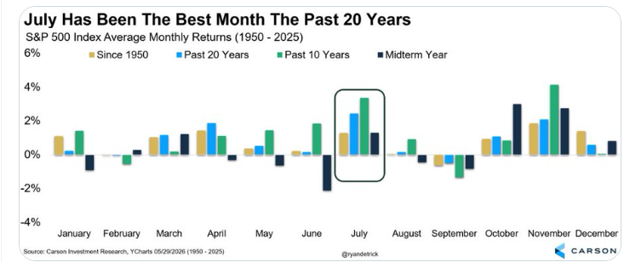

There is also some encouraging seasonal data. According to Ryan Detrick, Chief Market Strategist at Carson Group LLC, July has been the best-performing month for the U.S. stock market over the past 20 years.

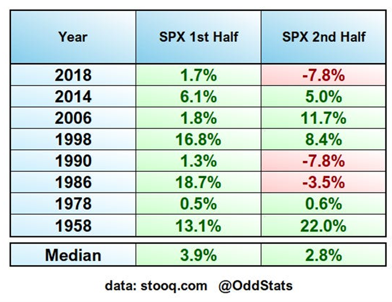

History also offers another reason for optimism. Research from OddStats shows that when the stock market posts a positive first half during a U.S. midterm election year, the second half has historically also generally been positive, with a median return of approximately 2.8%.

History also offers another reason for optimism. Research from OddStats shows that when the stock market posts a positive first half during a U.S. midterm election year, the second half has historically also generally been positive, with a median return of approximately 2.8%.

Of course, history doesn't guarantee future returns, but it does provide helpful context.

Is Market Leadership Starting to Broaden?

One of the more interesting developments we've been watching comes from Jim Bianco, President and Macro Strategist at Bianco Research LLC.

Over the past week, he stated, AI-related stocks have declined roughly 4.5%, while the rest of the market has actually risen by more than 2%. In other words, many of the companies outside the AI sector have begun outperforming even as AI leaders have pulled back.

It's far too early to draw any firm conclusions from a week of trading, but if this trend continues it could be a very healthy development. A market where gains are spread across more companies rather than concentrated in a handful of names is generally a stronger and more sustainable market.

We'll continue watching this closely.

The AI Bubble Narrative Continues...

As expected, every pullback in AI stocks has brought out predictions that we're witnessing another Dot-Com bubble.

What many of these comparisons ignore is one very important fact.

Unlike the late 1990s, today's AI leaders are generating substantial profits and cash flow.

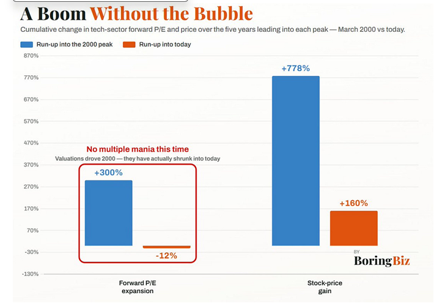

As Boring Biz recently noted:

"A lot of people continue to compare the AI cycle with the dot-com bubble, without realizing that today's run-up has been driven by fundamental earnings growth, while the 2000s was mostly hopes and dreams. Forward P/E (price/earnings) multiples in technology have actually contracted even as stock prices have gone up this time around."

That last point is particularly important.

Despite strong stock performance, technology valuations today are actually less expensive on a forward earnings basis than they were at the beginning of the year. Rising earnings—not simply investor excitement—have been driving much of the performance.

Despite strong stock performance, technology valuations today are actually less expensive on a forward earnings basis than they were at the beginning of the year. Rising earnings—not simply investor excitement—have been driving much of the performance.

That doesn't mean there won't be volatility. There always is. But it's a very different backdrop than the speculative environment of 2000.

My Thoughts

This is one of the reasons I've remained constructive on the AI theme.

The AI story isn't simply about exciting technology. It's about one of the largest capital investment cycles we've seen in decades. Companies are investing hundreds of billions of dollars into the physical infrastructure needed to support artificial intelligence—from semiconductors and memory chips to power generation, electrical equipment, networking, and data centres.

That creates opportunities well beyond just a handful of technology companies.

While markets will undoubtedly experience corrections along the way, I continue to believe the longer-term investment case remains compelling because it is being supported by real earnings growth, real capital investment, and businesses solving meaningful problems—not simply speculation.

My bold predictions for the Second Half of 2026

Inflation will likely prove lower than many investors currently expect. I believe June could ultimately mark the peak in this inflation cycle as temporary pressures begin to fade.

Interest rates are more likely to remain unchanged or move lower than higher. I would be surprised to see another rate hike this year if inflation continues to moderate.

A softer inflation backdrop could put rate cuts back on the table. If that happens, it would provide additional liquidity to the financial system—a backdrop that has historically been supportive for equities.

While volatility is always possible, I remain constructive on the second half of the year. Strong corporate earnings, continued AI investment, and the potential for easier monetary policy could all provide support for markets if our outlook proves correct.

Last year, I made several forecasts that challenged the prevailing narrative, including my view that tariffs would ultimately prove deflationary rather than inflationary. Those predictions proved to be correct. Once again, my outlook for the second half of 2026 runs counter to much of today's consensus, particularly on inflation and interest rates. Time will ultimately judge these forecasts, and I'll revisit them in a year's time. As always, investing requires adapting to new information, and my views will evolve as the evidence does.

Mark Ting is a registered Portfolio Manager at Foundation Wealth Partners. Foundation Wealth Partners LP is registered as a Portfolio Manager and Exempt Market Dealer in all Canadian provinces and the Yukon territory.