Back, Caught Up—and What Actually Matters Now

March 20, 2026

I just got back after being away for about a week.

When I travel, I generally try to disconnect from markets as much as possible-- step away, clear my head, and not get caught up in the day-to-day noise. But this time, that was harder than usual.

Even on a remote island, the headlines find you.

Between snippets of news, conversations with other travelers, and just general chatter about what’s going on in the world, it was clear something meaningful was unfolding. You could feel the uncertainty—even outside of financial circles.

So I knew when I got back, I’d need to spend some real time getting fully up to speed.

I had about 24 hours in transit, and I used that time to do a deep dive—listening to analysts, going through data, and trying to filter out what actually matters versus what just feels important in the moment.

What I Took Away After Catching Up

After spending a couple of days digging into this, here are the key takeaways.

1) Nobody Really Knows How This Plays Out

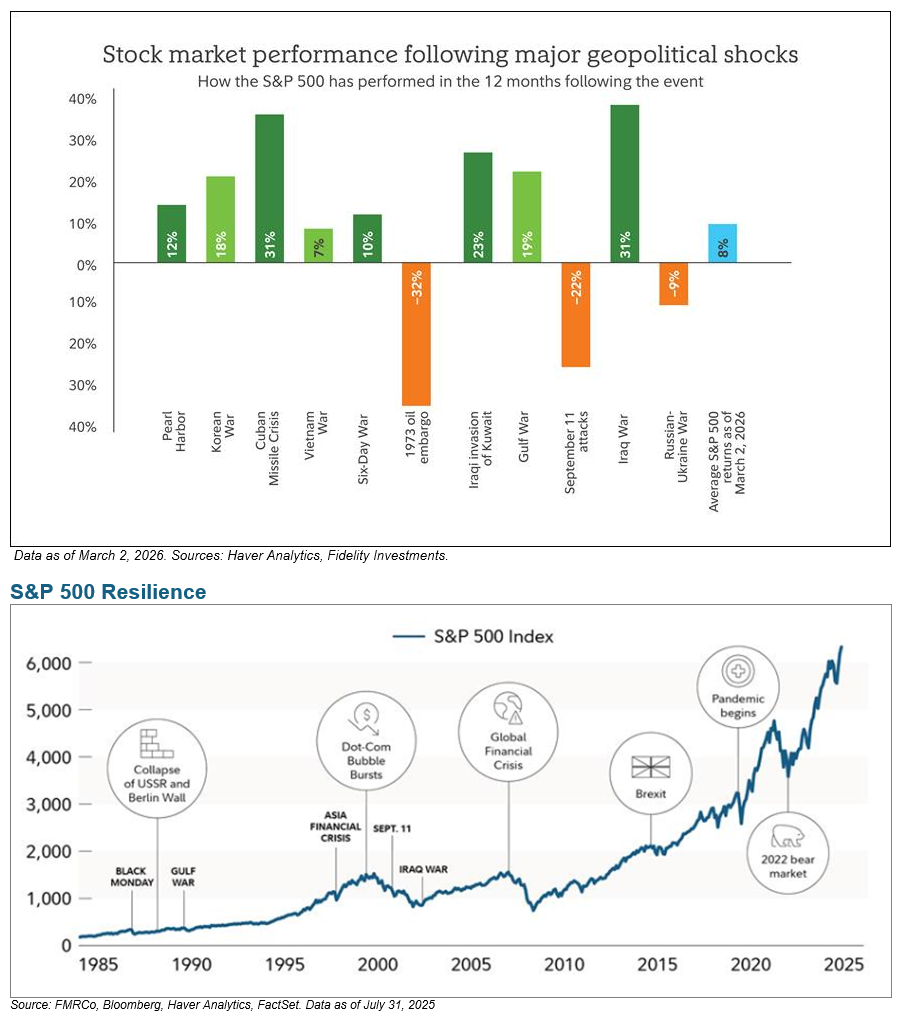

One of the clearest themes—across all the analysts I listened to—is that this situation is highly uncertain.

Even the most experienced geopolitical experts aren’t predicting outcomes with confidence. And that’s not a knock on them—it’s just the nature of these events.

They’re dynamic. They evolve quickly. And decisions are made behind closed doors.

So from an investment standpoint, trying to position portfolios based on specific geopolitical outcomes is extremely difficult—and often counterproductive.

2) Markets Are Not Behaving Like This Is a Crisis

This is important and a good sign.

If you just followed the headlines, you’d expect markets to be under significant stress.

But they’re not.

Equity markets have been relatively stable

Credit markets are calm

We’re not seeing widespread forced selling or panic

That doesn’t mean there’s no risk—but it does mean markets are not pricing in a worst-case scenario.

And markets are usually pretty good at sniffing that out.

3) Oil Is the One Signal That Matters

If there’s one variable that actually matters right now, it’s oil.

The reason is simple:

Oil directly impacts financial conditions.

When oil spikes sharply and stays elevated, it acts like a tax on the global economy—slowing growth, tightening conditions, and increasing recession risk.

Historically, when oil moves 50% above trend, it has often preceded economic slowdowns.

Right now, we’re elevated—but not at those levels.

So we’re in a watch zone, not a danger zone.

If oil stabilizes or declines → likely no major issue

If oil continues higher and stays there → that’s when risk increases

4) Liquidity Is Still Supportive

Liquidity is what drives markets.

Everything else—wars, trade disputes, political tension—only matters to the extent that it either adds or removes liquidity from the system.

This is the most important piece—and the one that markets seem to be focusing on.

Despite everything going on:

Central banks are not aggressively tightening

The banking system is still creating credit

Fiscal spending is still flowing into the system

Global liquidity (including China) is still expanding

That matters more than headlines.

In fact, one of the more interesting observations from what I reviewed is that even with negative news flow, markets have remained resilient—because liquidity hasn’t been pulled.

Historically, you don’t get sustained market declines without that. This is very good news.

5) Geopolitics Feels Big—But Often Isn’t (For Markets)

One of the more blunt—but accurate—points I came across:

“Nobody knows anything when it comes to geopolitics.”

That might sound extreme, but the idea is this:

Everyone has a framework

Everyone has an opinion

But very few have predictive accuracy

And more importantly:

Even if you could predict outcomes, it’s still hard to translate that into actionable investment decisions.

Most geopolitical events end up being noise for markets, unless they:

Disrupt commodities (like oil), or

Tighten liquidity

Ukraine was an example where it mattered—because it triggered a commodity shock.

This situation has yet to reach that level.

So Where Does That Leave Us?

Putting it all together:

We have a high-uncertainty geopolitical backdrop

Oil is elevated but not critical

Liquidity remains supportive

Markets are behaving in a relatively stable manner

Which leads to a fairly straightforward base case:

This is more likely to be a period of volatility than the start of a major downturn.

What We’re Doing

In this kind of environment, the biggest risk is overreacting.

Our approach remains consistent:

We are not making major portfolio changes based on headlines

We are watching oil and financial conditions closely

We are prepared to take advantage of volatility if opportunities arise

One of the key mindsets shifts here is this:

Instead of viewing market declines as something to fear, we view them as potential opportunities—provided the underlying fundamentals remain intact.

Right now, they do.

The U.S. government is also facing a potential policy crossroads

The U.S. government is also facing a potential policy crossroads

If this conflict drags on, it quickly stops being just a geopolitical issue and becomes an economic one. At that point, they’ll be forced to respond—likely through monetary or fiscal support to stabilize things at home.

And the timing matters.

This is a midterm election year, and Trumps approval ratings are in the gutter. For him to turn things around he can’t go into an election with high inflation, worsening affordability, and an ongoing conflict overseas.

Because of that, the incentives are pretty clear.

Many of the analysts I’ve spoken to believe we’ll see some form of de-escalation in the next couple of weeks. It may not be perfect, but it gives the administration a chance to claim progress and shift focus.

From there, the priority likely becomes bringing oil prices down—easing inflation and taking pressure off the economy.

And if that happens, a major source of market risk starts to come off the table and markets should rebound sharply.

Final Thoughts

If you step back, the most important takeaway is this:

Markets are being driven less by what’s happening—and more by what isn’t happening.

Liquidity hasn’t been pulled. Financial conditions haven’t tightened meaningfully. And as a result, markets are holding up.

That doesn’t mean we won’t see volatility. We likely will.

But volatility and risk are not the same thing.

We’ll continue to monitor things closely and update you as the situation evolves.